Page 124 - IRSEM_Main Book

P. 124

702. The Abstract Estimate: An abstract estimate is prepared in order to enable the authority

competent to give administrative approval to the expenditure of the nature and the

magnitude contemplated, to form a reasonably accurate idea of the Probable expenditure and

such other data sufficient to enable that authority to gauge adequately the financial prospects

of the proposal. Abstract estimates avoid the expense and delay of preparing estimates for

works in detail at a stage when the necessity or the general desirability of the works proposed

has not been decided upon by competent authority. An abstract estimate should contain a

brief report and justification for the work, specifications and should mention whether funds

are required in the current year and to what extent. It should also show the cost sub-divided

under main heads and sub-heads or specific items, the purpose being to present a correct idea

of the work and to indicate the nature of the expenditure involved. The allocation if each item

as between Capital, Development Fund, Open Line Works-Revenue, Depreciation Reserve

Fund and Revenue should be indicated.

Note: Administrative approval to a work or scheme should be accorded by the authority

competent to do so (vide paragraph 748), after a through examination of its necessity,

utility and financial propspects. See also rules in Chapter II of Indian Railway Financial

Code.

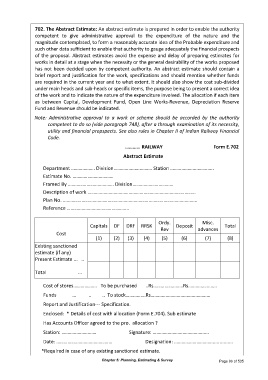

………… RAILWAY Form E.702

Abstract Estimate

Department ………………. Division…………………………. Station ……………………………..

Estimate No. ……………………………

Framed By ………………………………. Division……………………………

Description of work ……………………………………………………………………………

Plan No. ……………………………………………………………………………………………...

Reference …………………………………………..

Ordy. Misc.

Capitals DF DRF RRSK Rev Deposit advances Total

Cost

(1) (2) (3) (4) (5) (6) (7) (8)

Existing sanctioned

estimate (if any)

Present Estimate ... ..

Total ...

Cost of stores………………. To be purchased ..Rs……………………Rs…………………..

Funds ... .. .. To stock…………….Rs…………………………………………

Report and Justification--- Specification.

Enclosed: * Details of cost with allocation (Form E.704). Sub estimate

Has Accounts Officer agreed to the pro. allocation ?

Station: ………………………. Signature: ……………………………………...

Date: ……………………………………… Designation: …………………………................

*Required in case of any existing sanctioned estimate.

Chapter 5: Planning, Estimating & Survey Page 96 of 535